Battery recycling has made enormous strides in recent years. Regulations are in place, and capacity is growing. What is often overlooked is that the crucial step happens before the shredder—during disassembly. This article examines an underestimated bottleneck, pack architectures that hinder the circular economy, and an approach that turns automated robots into the solution.

In the public debate, battery recycling has gained significant momentum in recent years: The regulatory framework is in place, capacities are growing, and interest in raw materials is high. What is rarely discussed, however, is: The crucial step does not take place in the smelting furnace or during hydrometallurgical processing—it happens before that, during disassembly. Before a high-voltage battery can be recycled, it must be dismantled: into modules, cells, copper and aluminum components, circuit boards, and plastics. This step plays a decisive role in determining the quality of the resulting material stream.

Three challenges are particularly critical: the high physical effort involved, the significant safety requirements when handling high-voltage systems—and a skilled labor market that works against manual scaling.

The startup R3 Robotics has turned this into a mission: Automating disassembly not only solves a process issue; it creates the conditions for a functioning circular economy.

Software-enabled hardware: The R3 Robotics approach

R3 Robotics was founded by Antoine Welter and Xavier Kohl. Kohl earned his Ph.D. in Chemical Soft Robotics at ETH Zurich; Welter comes from a background in strategy consulting and B2B sales, but has focused on battery systems and the circular economy for years. Their core premise: The key lies not in the recycling process itself, but in the clean material stream leading up to it—and that can only be achieved through intelligent disassembly.

To this end, the company operates a fully certified recycling facility in Kuppenheim near Karlsruhe. A decision that initially met with resistance from investors—investors tend to favor “asset-light models,” Welter admits. But without their own facility, the founders are convinced, models cannot be trained and processes cannot be tested on an industrial scale. There is also a practical sales argument: in practice, European industrial customers often work exclusively with certified facilities. The site serves as both a demonstration and development center; customers want to see the technology before they invest. In 2023, R3 Robotics won the European Innovation Council Accelerator.

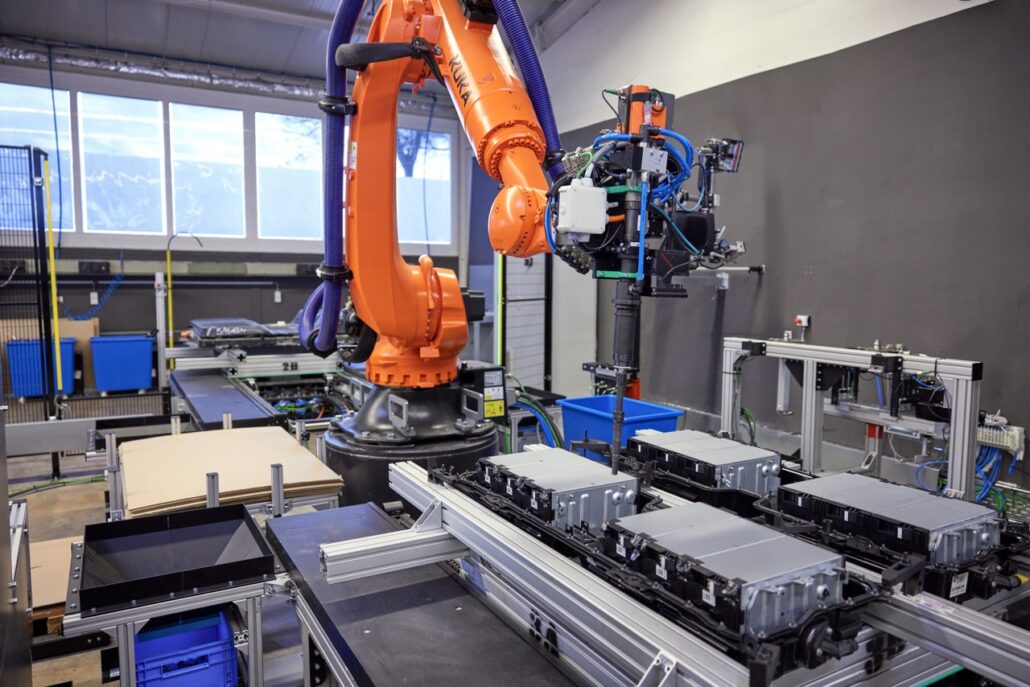

The founders describe the technical core as “software-enabled hardware”—a term chosen deliberately. Robots alone are not enough. Customized end-effectors are needed—that is, grippers and tools on the robot arm—tailored to the specific pack architecture. Combined with computer vision, the system autonomously recognizes which package is on the tool carrier and initiates the corresponding disassembly process.

„Robotics alone does not solve the problem. It requires customized end-effectors, computer vision, and the process knowledge of how software and hardware work together. “ — Antoine Welter, co-founder of R3 Robotics

R3 Robotics internally refers to these combinations of tool hardware and software intelligence as “skills.” Two to three new ones are developed each quarter, as pack architectures are constantly changing. The system is dual-configurable, meaning it is equipped to handle two different pack types simultaneously, and flexibly processes a wide variety of battery types. This reflects real-world conditions at recycling facilities: packs arrive in mixed batches, not sorted.

The nominal system capacity (nameplate capacity) is approximately 1,600 tons per year with 1.5-shift operation. In the medium term, R3 Robotics is focusing on a Robotics-as-a-Service model: The systems are to be operated directly at the customer’s site—at recyclers or OEMs—because battery logistics are a significant cost factor and the regulatory requirements for transporting high-voltage batteries quickly undermine the business case.

Why manual disassembly is no longer feasible

Battery disassembly is physically demanding. Welter has experienced this firsthand:

„I once disassembled three batteries in a single day. I’m 6 feet 6 inches tall, weigh 220 pounds, and I’m not the type to shy away from hard work. It’s really, really hard work.” — Antoine Welter

Vehicle batteries are simply not designed for manual disassembly. Bolted and glued packs require considerable force, lifting modules pushes the limits of occupational safety guidelines, and the entire process takes place in close proximity to high-voltage systems. The robot has a structural advantage here: It never gets tired, never loses focus, and if something does go wrong, an end-effector burns out—not a human hand.

Another factor is a scaling problem that is already acute in the U.S. and is becoming increasingly noticeable in Europe: a shortage of skilled workers. Welter reports from conversations with American recyclers that qualified personnel are migrating to the booming data center sector—with correspondingly better pay. Without skilled workers, manual scaling becomes impossible, no matter how much the volume increases.

Second life first, recycling last

R3 Robotics postions itself not as a recycler, but as an upstream process provider: disassembly, sorting, condition assessment. The result is clean material streams for various uses—intact modules for second-life applications, copper, aluminum, plastics, and battery management systems for reuse. Only what is truly no longer usable goes to the shredder.

R3 Robotics has implemented this tiered model—reuse, then second life, then recycling—in a project with Amazon: Batteries from Rivian vehicles in Amazon’s delivery fleet are disassembled. Intact modules are first used in stationary energy storage systems for solar installations; after all, Amazon is one of the world’s largest solar operators. Only at the end of this second life are the materials sent for recycling. Clean disassembly is the enabler for all three stages.

Growing market, growing pressure

The market dynamics are clear: According to Global Market Insights, the European market for lithium-ion battery recycling is estimated at around $2 billion in 2025, with an expected annual growth rate of around 20 percent through 2034. According to Fraunhofer ISI, European pre-treatment capacity has doubled to around 300,000 tons per year by the end of 2024. By 2040, Strategy& (PwC) expects 6 million tons of end-of-life batteries in the European market alone.

On the demand side, the EU Battery Regulation (2023/1542) sets the framework: It requires manufacturers to take back end-of-life packs and mandates specific recovery targets: 80 percent for lithium by 2031, 95 percent for cobalt, copper, nickel, and lead. Starting in 2031, minimum percentages of recycled material in new batteries will apply (including 16% cobalt, 6% lithium, and nickel). Against this backdrop, the quality of pre-treatment and disassembly is likely to become a decisive competitive factor in European battery recycling.

Strategy& (PwC) expects investments of over 2 billion euros in the European recycling market by 2030 and a revenue potential of up to 8 billion euros by 2040. Recycled material could cover up to 30 percent of the lithium, nickel, and cobalt demand for European battery cell production by 2035—provided that processing capacities for black mass are established in Europe itself.

The cell-to-pack question

While automation of disassembly is advancing, a new challenge is looming on the horizon: newer pack architectures, particularly cell-to-pack (CTP) designs. In CTP, cells are integrated directly into the pack without a module level—this saves weight and costs during vehicle operation but makes disassembly considerably more complicated. Reusing individual cells is practically impossible with such architectures.

The challenge becomes even greater with heavily encapsulated packs. When cells and structural components are firmly encapsulated together, the only option left is often the shredder.

„With packs that are difficult to disassemble, the payment flow reverses: It is not the recycler who pays for the material, but the OEM who pays for disposal. Many recyclers do not accept such packs at all.” — Antoine Welter

Design for Circularity is already a topic in the industry—but is primarily treated internally by OEMs as a matter of cost optimization: How do I design the pack so that its take-back costs me less? R3 Robotics is working with several OEMs on the question of how packs can be designed to be more disassembly-friendly from the outset, and has found that the willingness to engage in dialogue has increased significantly there. The economic pressure is now concrete enough.

Europe: Regulation is just the beginning

Europe has a structural advantage in the global context: a consistent regulatory framework and a deep-rooted industrial tradition. China dominates in terms of volume and cost efficiency, while the United States still lacks the industrial infrastructure for high-quality recycling in many areas. The European approach—regulate first, then implement industrially—can work. But only if the crucial next step succeeds: anchoring black mass processing capacities in Europe instead of exporting them to Asia.

Those who perform clean dismantling produce high-quality black mass. Those who also process the high-quality black mass themselves close the loop—and achieve the raw material independence that Europe strives for. Both require that the step before the shredder be taken seriously.

R3 Robotics’ goal is clear—but Welter isn’t just looking at his own company. What he observes in the industry makes him optimistic: collaboration along the battery value chain is becoming a reality. OEMs, recyclers, technology providers, and research institutes, which for a long time tended to operate in parallel, are actually coming together. What used to be mere rhetoric—we must work together—is increasingly becoming a lived reality, says Welter. That, he argues, is the actual prerequisite for Europe to become competitive in the battery circular economy.

Disassembly is not the end of the story—but its beginning.

Sources & data:

Strategy& / PwC (2024): European Battery Recycling Market Analysis. https://www.strategyand.pwc.com/de/en/industries/automotive/recycling-european-battery.html

Global Market Insights (2025): Europe Lithium-Ion Battery Recycling Market. https://www.gminsights.com/industry-analysis/europe-lithium-ion-battery-recycling-market

Fraunhofer ISI / Statista (August 2024): Batterierecycling in Europa nimmt weiter Fahrt auf: Recycling-Kapazitäten von Lithium-Ionen-Batterien in Europa. https://www.isi.fraunhofer.de/de/blog/themen/batterie-update/lithium-ionen-batterie-recycling-europa-kapazitaeten-update-2024.html

EU-Rat (July 2023): Verordnung (EU) 2023/1542 über Batterien und Altbatterien. https://eur-lex.europa.eu/legal-content/DE/TXT/?uri=CELEX:32023R1542

MDPI Batteries (June 2025): Progress, Challenges and Opportunities in Recycling Electric Vehicle Batteries. https://www.mdpi.com/2313-0105/11/6/230

Quotes and company information: Interview with Antoine Welter, co-founder of R3 Robotics, held by Battery News (March 2026). The transcript is available to the editorial staff.